Bookkeeping

BookkeepingCOMMERCIAL FINANCE

Pinnacle Road specialise in a number of commercial finance options.

- Commercial Property

- Unsecured Business Loans

- How do unsecured business loans work?

- Cash Flow Finance

- Trade Finance

- Debtor Finance

For investors and owner occupiers we offer commercial loans for retail, office and industrial freehold. We also offer development finance for retail and industrial units, and finally we facilitate the refinancing of commercial property loans for better interest rates and expired loan terms.

Commercial property finance is a loan to be used for commercial property such as a factory, shopfront, office block or other industrial land. You could use a commercial property loan to buy a new or existing commercial property, or to do any future development or renovation. These types of loans are usually taken out by businesses rather than individuals.

Commercial property loans also require a deposit, but the percentage will depend on the type of loan (for example, a low doc loan will require a bigger deposit) and the type of property used as security. Put simply, a commercial property loan is a mortgage where the property that is used as security is anything other than a residential property.

ADVANTAGES

- Lower interest rates than other types of finance

- Property acts as security for the loan – other security is not needed

- Options are available for bad credit

DISADVANTAGES

- More documentation required than other loan types

- Slower than other loan types

|

Unsecured business loans are loans provided for a fixed period that are not backed by property, equipment or another form of collateral.

Because they are not secured by collateral, unsecured business loans are supported in another way, often by business cash flows in combination with the borrower’s creditworthiness. |

ADVANTAGES

- A set payment structure

- Limited paperwork

- You can get an unsecured loan even if you have bad credit

- Suitable for a wide range of purposes

DISADVANTAGES

- Higher rates than longer-term loans

- Daily or weekly payment can prove difficult for some businesses

Most unsecured business loans are short-term. They are short-term due to the fact that they carry more risk to the lenders.

Short-term unsecured loans often come with factor rates instead of interest rates. A factor rate is a number that, when multiplied by your total loan amount, tells you how much you need to pay back the lender. It’s expressed as a figure such as 1.15. So, if your loan is for $100,000 and your factor rate is 1.15, you need to pay $115,000.

In addition, short-term unsecured business loans often have either weekly or daily repayments. Breaking repayments down into smaller amounts can make it easier to manage your cash flow.

Because of the need for daily or weekly repayments, short-term unsecured business loans are best suited to businesses that have a stable and regular revenue.

Here is an example of how an unsecured loan could work for you:

An unsecured loan example

- You need to borrow $100,000.

- Your factor rate is 1.18 factor over 12 months with weekly repayments.

- You will need to repay a total of 1.18 * $100,000 = $118,000.

- Dividing $118,000 by 52 weekly payments means that you will make repayments of $2269 per week.

Do you Qualify?

ADVANTAGES

- Trading for a minimum of 6 months

- Revenues of at least $5,000 per month

DISADVANTAGES

- Start-up businesses

- Businesses with less than $5,000 in monthly revenue

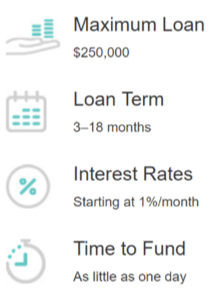

One of our major lending partners specialises in unsecured small business loans online, Pinnacle Road can broke cash flow loans up to $250,000 with instant approval across a 6-12 month term. Pinnacle Road also offer flexible funding with no hidden fees, so you know exactly what you’re getting when you apply – just an easy to understand interest rate applied against your outstanding balance.

Our partner analyses your business’ data and provides commercial funding that is designed to help you grow from strength to strength in a competitive marketplace. At the present, our partner is happy to fund between $3,000 and $250,000; However, if you need more than $250,000, please contact the Pinnacle Road team.

Markets across the globe are becoming more accessible and cross-border transactions are now part of everyday life for many SMEs. This has led to trade finance becoming an increasingly important business tool.

Trade Finance is a form of working capital; the term commonly refers to the financing of cross-border, import/export transactions. For an importer it means receiving funding to pay a supplier and allow time for the goods to be received, sold and turned into cash.

For an exporter it provides working capital until the overseas customer pays for the goods or services that have been delivered. Exporters typically utilise export factoring or bill facilities as the primary means of financing overseas trading, which may be supported by a letter of credit to secure the transaction.

Our Lenders Trade Finance offerings include:

- Tradeline– A fast and simple line of credit helping businesses purchase goods

- Import Finance– Helping businesses improve their purchasing power and cash flow with a complete, end to end funding solution

- Export Finance– Providing business access to additional working capital and improving cash flow by advancing funds against export invoices

- Export Finance (EFIC)– Leveraging our relationship with EFIC, we can support more businesses and help them achieve their goals in international markets

What is debtor finance?

Debtor Finance is, quite simply, a line of credit linked to and secured by your outstanding accounts receivable.

If your business supplies products or services to other businesses on standard trade credit terms, Debtor Finance can help.

There are a number of variations in how the service is delivered, ranging from Confidential Invoice Discounting (for larger, more sophisticated businesses with a dedicated finance department) to the option of full management of accounts receivables (which allows many of our smaller clients to focus on growing their businesses rather than chasing outstanding invoices).

What are the benefits of debtor finance?

It is a powerful standalone business finance facility, which helps because:

- As your business grows the facility grows with it

- Unlike a traditional bank overdraft, there is generally no need for real estate security

- It is a standalone facility that can sit alongside other business borrowings (such as overdrafts, term loans, and asset finance)

- It helps you grow your business and increase purchasing power through improved cash flow

- There are no capital repayment requirements

How does debtor finance work?

You invoice your client directly and upload the invoice to us at the same time. Within 24 hours our lender will pay 80% of the value of approved invoices, less our fees. The remaining 20% becomes available to you when the invoice is paid in full.

Imagine you are a furniture importer who wholesales to other businesses.

You buy a chair for $20 and sell it for $50, BUT you only had $20 and have to wait to get paid (possibly 45 to 60 days) before you can buy and sell another chair.

No problem, our lenders can give you up to $40 against the invoice within 24 hours (with the balance on full payment by the debtor), meaning that you can immediately go and buy two chairs for your $40 and sell them for $100…

Now we can give you $80 against the second invoice and you can buy four chairs and so on. The math speaks for itself!

This is a very simple example, but debtor finance is just that – simple.

Without A Debtor Finance Facility

- Buy a chair for $20

- Sell the chair for $50

- Wait for payment to buy another chair

With A Debtor Finance Facility

- Buy a chair for $20

- Sell the chair for $50 but rather than wait to get paid, receive $40 the next day, meaning you can

- Buy 2 more chairs

Will debtor finance help my business?

If you answer “Yes” to these 3 questions, your business could benefit from a debtor finance facility.

- Do you sell products or services to other businesses on standard trade credit terms?

- Are your invoices issued for delivered goods or completed services (i.e. not issued on a progress claim/milestone basis)?

- Does your business have an annual turnover greater than $200,000?

For more information about how we can help your business please contact Pinnacle Road.

Let's Chat

We’d love to hear from you. If you have a question, need more information or just want to organise a coffee, drop us a message below.

contact us

Our office is located in South Yarra. We are mobile based and come to you anywhere, any day, anytime.

- The Loft - Level 2, 627 Chapel St, South Yarra, VIC 3141

- info@pinnacleroad.com.au

OUR partners